If you’ve ever driven past a house with an overgrown lawn and a mailbox stuffed with letters, there’s a chance that home is in pre-foreclosure. And for real estate investors who know what to look for, that house represents something the open market rarely offers: a motivated seller, a discounted price, and a real opportunity.

This guide breaks down exactly what pre-foreclosure means, how to find these properties, how to approach the seller, and what to expect when you buy one. Whether you’re a first-time investor or a seasoned buyer looking to sharpen your deal-finding strategy, this is one process worth understanding inside and out.

What Is Pre-Foreclosure? (And Why Smart Investors Pay Attention)

Pre-foreclosure is the period that begins when a homeowner falls behind on mortgage payments and the lender files a public notice of default, but before the home is actually repossessed or sold at auction.

Think of it as the warning stage. The homeowner is behind. The bank has officially put them on notice. But there is still time for the situation to resolve, and that window is where the opportunity lives.

During pre-foreclosure, the homeowner has a few options: catch up on payments, refinance, sell the home, or negotiate a short sale with the lender. For investors, the “sell the home” option is the one that matters most.

The Foreclosure Timeline at a Glance

Understanding where pre-foreclosure fits in the broader foreclosure process is important:

- Missed payments (30 to 90 days): The homeowner falls behind. No public action has been taken yet.

- Notice of Default (NOD): The lender files a public notice, officially starting the pre-foreclosure clock.

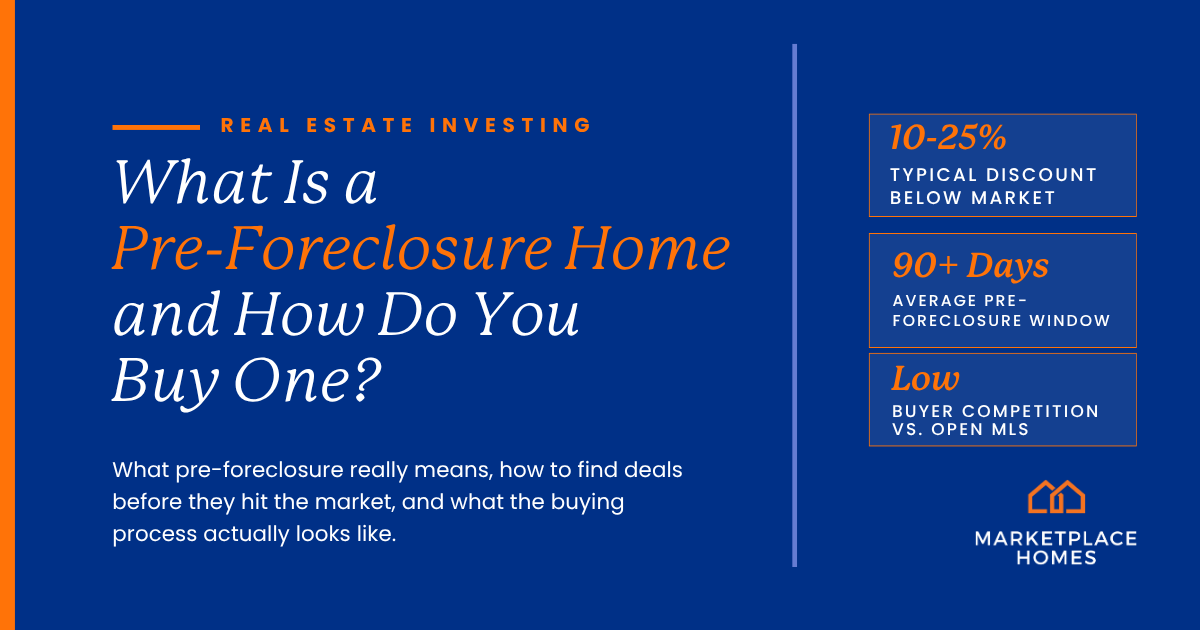

- Pre-foreclosure period: The homeowner has time to resolve the debt or sell the property. This window varies by state, typically 90 days to 6+ months.

- Foreclosure auction: If no resolution is reached, the home goes to auction.

- REO (Real Estate Owned): If the home doesn’t sell at auction, the bank takes it over as a bank-owned property.

Pre-foreclosure sits in that second and third stage, after the notice is filed but before the auction happens. It is a defined, time-limited window, which is exactly why investors who know how to move quickly can find deals here that the average buyer never sees.

Why Pre-Foreclosure Properties Appeal to Investors

The appeal comes down to a combination of motivation and timing.

Motivated Sellers

A homeowner in pre-foreclosure is dealing with a financial crisis. Foreclosure will destroy their credit for years and leave them with nothing to show for whatever equity they had built. Many sellers in this position are genuinely willing to accept a below-market offer in exchange for a fast, clean close that stops the clock.

That is not exploitation. It is a transaction that can benefit both parties. The seller gets out of a bad situation with their credit partially intact. The investor gets a property at a price that allows for profit or strong cash flow.

Below-Market Purchase Price

Because the seller is often motivated and under time pressure, pre-foreclosure homes frequently trade at a discount compared to comparable properties. The discount varies widely depending on the seller’s equity, the local market, and how far along the foreclosure process has moved, but deals in the 10% to 25% below-market range are not uncommon.

Less Competition Than the Open MLS

Pre-foreclosure deals are not listed on Zillow. They are not sitting in your agent’s feed. Finding them requires a little more effort, which means fewer buyers are competing for the same properties. Less competition means more negotiating leverage.

Potential for Equity or Cash Flow

If you are a buy-and-hold investor, a pre-foreclosure property purchased below market gives you immediate equity and the potential for strong rental returns. If you are a fix-and-flip investor, that same discount creates room for renovation costs and still leaves profit on the table.

How to Find Pre-Foreclosure Properties

This is where most investors get stuck. Pre-foreclosure homes are not on the MLS, and they are not always easy to find. But the data is out there if you know where to look.

1. Public Records and the County Courthouse

When a lender files a Notice of Default, it becomes part of the public record. Most counties record these documents and make them searchable, either online or in person at the courthouse. This is the most direct source of pre-foreclosure data, but it requires some legwork to compile and track.

Search your county recorder or assessor’s website for “notice of default” or “lis pendens” filings. Lis pendens is a Latin term meaning “lawsuit pending” and is used in many states to signal that a legal action involving the property has been filed.

2. Online Property Data Platforms

Several platforms aggregate foreclosure and pre-foreclosure data from public records and make it easier to search and filter. Some of the most commonly used include:

- PropStream: One of the most comprehensive tools for investor-focused property data, including pre-foreclosure filters.

- ATTOM Data Solutions: Institutional-grade property data with pre-foreclosure and distressed property flags.

- RealtyTrac: One of the original foreclosure listing databases, now part of ATTOM.

- com: Consumer-friendly interface with pre-foreclosure, auction, and REO listings.

These platforms typically charge a monthly subscription fee, but for active investors, the cost is easily offset by a single good deal.

3. Driving for Dollars

Low-tech, but still effective. Pre-foreclosure homes often show visible signs of distress: deferred maintenance, overgrown landscaping, accumulated mail, or tarps on the roof. Driving target neighborhoods and noting addresses of neglected properties can surface opportunities that don’t appear in any database.

4. Working with a Real Estate Agent Who Specializes in Distressed Properties

An experienced investor-focused agent can have access to pre-foreclosure data through MLS systems that flag distressed properties or through relationships with attorneys, lenders, and title companies who see these situations early.

At Marketplace Homes, we work with investors across the country and can help surface off-market and distressed opportunities in the markets where we operate.

5. Direct Mail Campaigns

Once you have a list of properties in pre-foreclosure through public records or a data platform, you can run a direct mail campaign targeting those homeowners. A short, sincere letter that acknowledges their situation and explains that you are a cash buyer can generate responses. Response rates are low, but the quality of the leads that do respond tends to be high.

6. Probate and Estate Sales

Properties going through probate (when a homeowner passes away and the estate must be settled) can sometimes overlap with pre-foreclosure situations, especially when the estate cannot maintain mortgage payments. These are worth watching in parallel.

How to Approach a Pre-Foreclosure Seller

This part matters as much as finding the deal. How you approach the homeowner will determine whether you get a conversation or a door slammed in your face.

Lead with Empathy, Not Urgency

The seller is going through something hard. They may feel embarrassed, overwhelmed, or defensive. Do not open with a lowball offer or create artificial pressure. Start by acknowledging the situation and asking if they would be open to exploring options together.

Know What the Seller Needs

Not every pre-foreclosure seller is motivated purely by price. Some want a fast close. Some need extra time to move. Some are primarily trying to protect their credit. The more you understand what the seller actually needs, the better positioned you are to structure a deal that works for both parties.

Understand the Equity Position Before You Meet

Before you approach a seller, pull the property details. What do they owe on the mortgage? What is the home worth in current condition? What is the lender’s timeline? If the seller owes more than the home is worth, you may be dealing with a short sale situation, which involves the lender approving the sale price at a discount. That is a different process with different timelines.

Move Quickly But Don’t Rush the Seller

Pre-foreclosure deals have a built-in deadline, but pressuring the seller to decide before they are ready often backfires. Move efficiently on your end, have financing ready, know your numbers, and make it easy for them to say yes.

What the Buying Process Looks Like

Buying a pre-foreclosure home is more similar to buying a conventional property than many investors expect, but there are a few key differences to be aware of.

Step 1: Make an Offer

Once you have done your homework on the property value and the seller’s situation, you submit an offer directly to the homeowner. This is a standard purchase and sale agreement. There is no auction, no bank to negotiate with initially, just you and the seller.

Price it to work for both parties. If the home is worth $250,000 in market-ready condition and needs $30,000 in repairs, an offer in the $190,000 to $200,000 range may still net the seller a meaningful outcome while giving you workable margins.

Step 2: Title Search

A thorough title search is non-negotiable on any pre-foreclosure purchase. Distressed properties can carry liens, unpaid taxes, HOA arrears, second mortgages, mechanic’s liens, and more. You need to know exactly what you are buying and what obligations attach to the property before you close.

Step 3: Inspection

Pre-foreclosure homes are often deferred on maintenance. Budget for it. Get a full inspection and use the findings either to negotiate price or to set accurate renovation expectations.

Step 4: Negotiate and Close

If the numbers still work after inspection and title review, move to close. Cash buyers have a significant advantage here because lender delays can be fatal to a pre-foreclosure deal if the auction date is approaching. Many investors either pay cash or have hard money financing in place for speed.

What About the Lender?

If the seller owes less than the property is worth, the lender does not need to be involved in approving your purchase price. The seller pays off the mortgage at closing with the proceeds. If the seller owes more than the property is worth (upside down), you are in short sale territory, and the lender will need to approve the discounted payoff. Short sales add weeks or months to the timeline and introduce a layer of unpredictability, but they can still result in strong deals.

Risks to Know Before You Buy

Pre-foreclosure deals carry real risk. Going in clear-eyed is the only responsible way to approach them.

The Deal Can Fall Apart

The seller can catch up on payments, refinance, or simply change their mind at any point before closing. Pre-foreclosure deals fall through more often than conventional listings. Have a pipeline of leads so no single deal feels make or break.

Title Issues Are Common

As mentioned, distressed properties frequently carry title complications. Never skip the title search, and always use a reputable title company with experience in distressed properties.

Property Condition Is Often Unknown

If the homeowner has been financially distressed, the property has likely been deferred on maintenance. In some cases, sellers remove fixtures or appliances before vacating. Budget for the unexpected.

Financing Can Be a Challenge

Traditional lenders are often slow. If you are using conventional financing, the closing timeline may not align with the pre-foreclosure window. Cash or hard money financing gives you more control over timing.

Emotional Complexity

These deals involve real people in difficult situations. That can add complexity to negotiations and sometimes to closings. Work with professionals (agents, attorneys, title companies) who understand distressed transactions.

Pre-Foreclosure vs. Foreclosure Auctions vs. REO: What’s the Difference?

It’s worth being clear on where pre-foreclosure fits relative to the other stages of the foreclosure process, since investors often confuse them.

| Pre-Foreclosure | Foreclosure Auction | REO (Bank-Owned) | |

|---|---|---|---|

| Who you deal with | Homeowner directly | County / trustee | Bank / lender |

| Negotiation possible? | Yes | No | Limited |

| Inspection allowed? | Yes | Usually no | Usually yes |

| Title clarity | Requires title search | Can inherit liens | Usually clean |

| Competition level | Low to moderate | High | Moderate to high |

| Financing options | Cash, hard money, conventional | Cash only (most states) | Cash or conventional |

Is Pre-Foreclosure Right for Your Investing Strategy?

Pre-foreclosure works best for investors who:

- Have cash or fast financing available

- Are comfortable with some deal uncertainty (leads fall through, situations change)

- Can move quickly when the right property comes up

- Have the patience to build a lead pipeline over time rather than expecting instant results

- Operate in or are familiar with a specific market

It is less ideal for investors who need a predictable, plug-and-play acquisition process or who are not yet familiar with due diligence on distressed properties.

If you are newer to the distressed deal space and want to start building a portfolio without taking on renovation risk, turnkey new construction is often a smarter starting point. You get market-rate or above cash flow from day one, no rehab, and a clear title. Pre-foreclosure is a great long-term arrow to have in your quiver, but it is not the only way to build wealth through real estate.

The Bottom Line

Pre-foreclosure investing is not glamorous, and it is not passive. It requires patience, consistency, and the ability to navigate human situations alongside financial ones. But for investors who put in the work, it offers access to deals that the average buyer never sees, often at prices that create real, durable equity.

The formula is straightforward: find homeowners who need out, approach them with empathy and a clear offer, and execute quickly. Do that consistently in a market you understand, and pre-foreclosure becomes one of the most reliable deal sources in your investing playbook.